The same engineering-based methodology a $5,000 firm runs — software-applied per IRS Pub. 5653 and the Cost Segregation ATG. Residential 1–4 unit rentals up to $1M depreciable basis. $499 per study. Delivered same day.

A cost segregation study is an IRS-recognized tax strategy that breaks a residential rental property's depreciable basis into shorter-life asset categories — 5-year personal property and 15-year land improvements instead of the standard 27.5-year residential schedule. The accelerated depreciation produces larger Year-1 tax deductions. The IRS describes this methodology in Publication 5653 (Cost Segregation Audit Techniques Guide).

AI cost segregation applies that same methodology using software instead of an on-site engineer. The AI engine collects property data from public records, satellite imagery, and listing sources; classifies the building's components by tax recovery period using engineering-based rules; and produces the same depreciation schedules a traditional study would produce — at a fraction of the cost and time.

For residential 1–4 unit rentals within the $1M depreciable basis scope, the component classifications follow the same IRS-aligned principles a traditional engineering firm applies: kitchen cabinets and appliances reclassified to 5-year personal property, driveways and landscaping to 15-year land improvements, the building shell remaining on the 27.5-year residential schedule.

Four steps from address to filing-ready report. No site visit. No multi-week wait.

Address + acquisition price + closing date. The AI agent fetches everything else from public records.

Component-level engineering analysis classifies assets by recovery period — 5-year, 15-year, 27.5-year. Methodology aligned with IRS Pub 5653.

Quick review of the AI-extracted property facts (square footage, build year, structural type). Edit anything that's off.

Filing-ready PDF + Excel with depreciation schedules, Form 3115 package (look-back studies), recapture analysis, and IRS-citable methodology.

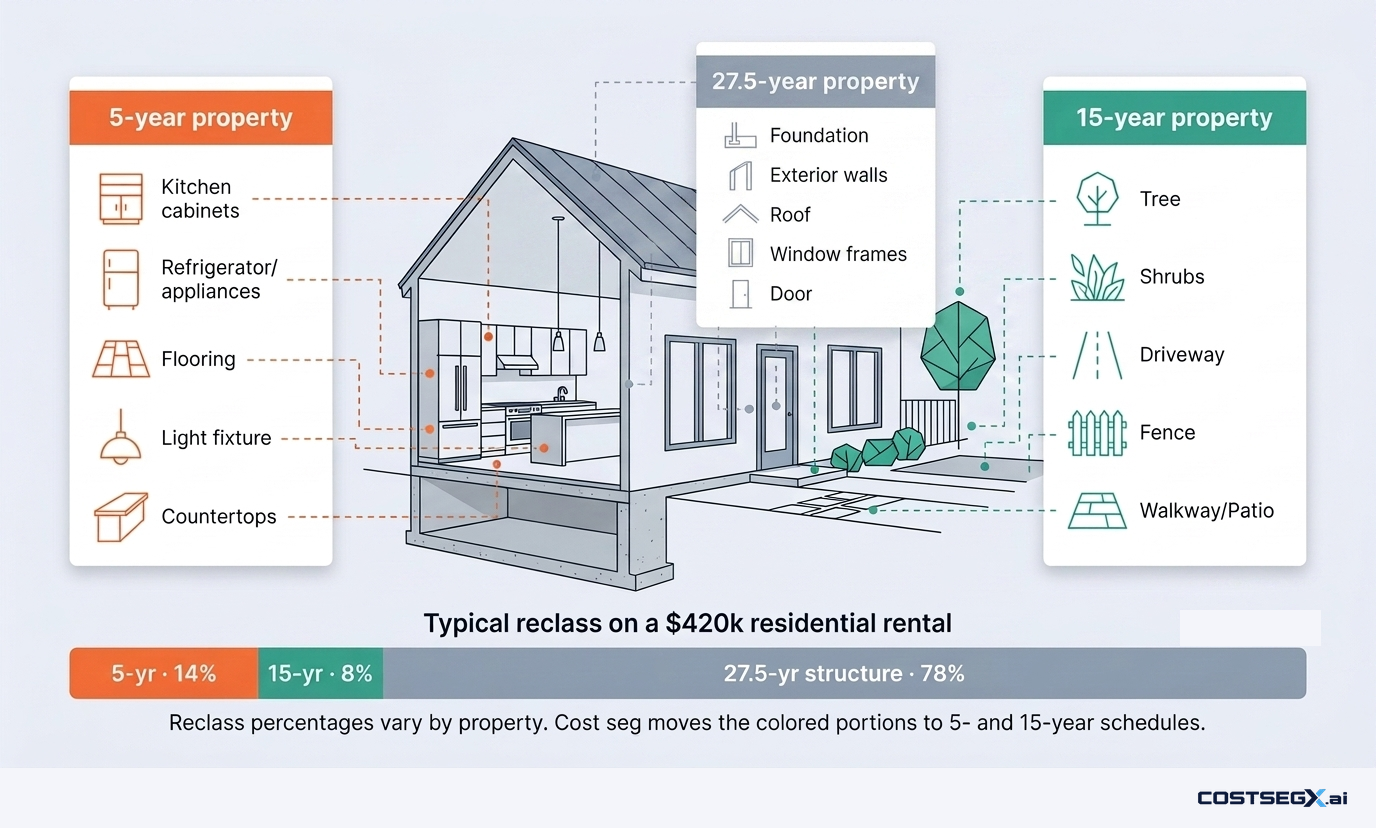

Cost segregation breaks the property's depreciable basis into faster recovery periods. A typical residential rental has roughly 22% of basis sitting in components that qualify for 5-year and 15-year schedules — the rest stays on the standard 27.5-year residential schedule.

Illustrative example based on a $420,000 residential rental. Reclass percentages vary by property type, age, and construction. Your CostSegX report calculates the exact split for your specific property.

Both produce IRS-aligned studies. The differences come down to scope, cost, and time to deliverable. Pick the right tool for the property in front of you.

| Dimension | Traditional engineering study | AI cost segregation (CostSegX) |

|---|---|---|

| Cost | $5,000–$15,000 | $499 flat fee |

| Time to deliverable | 4–8 weeks | Minutes after data confirmation |

| On-site inspection | Required | Public records + imagery + listing data |

| Property type | All scopes | Residential 1–4 unit, ≤$1M basis |

| Methodology | Engineering-based per IRS ATG | Engineering-based per IRS ATG |

| Output format | PDF + schedules | PDF + Excel + schedules |

| Form 3115 included | Usually extra fee | Always included |

| CPA-ready | Yes | Yes |

Methodology comparison applies to residential 1–4 unit properties within the $1M depreciable basis scope. Outside that scope, on-site inspection adds value AI cannot replicate.

Worked end-to-end so you can see how a typical residential rental's basis breaks out under the engineering-based methodology. Numbers below are illustrative — your actual study reflects your specific property.

| Category | % of Basis | Amount | Year 1 Deduction |

|---|---|---|---|

| 5-year personal property (appliances, flooring, cabinetry, fixtures, lighting, window treatments) | 14% | $58,800 | $58,800 (100% OBBBA bonus) |

| 15-year land improvements (driveway, fencing, landscaping, patio, walkways) | 8% | $33,600 | $33,600 (100% OBBBA bonus) |

| 27.5-year real property (foundation, framing, roof, exterior walls, HVAC, plumbing, electrical) | 78% | $327,600 | $5,956 (half-year convention) |

| Total Year-1 deduction | $420,000 | ~$98,400 |

Estimated Year-1 tax savings: ~$36,400

At a 37% combined federal+state marginal rate. Without cost segregation, the same property would generate ~$2,825 in Year-1 tax savings on the straight-line 27.5-year schedule — a ~13× difference in Year-1 deduction value.

Illustrative example. Reclassification percentages, OBBBA bonus eligibility (both acquired AND placed in service on or after January 19, 2025), tax bracket, and recapture timing all vary by property. CostSegX is a software platform, not a CPA firm; consult a qualified tax professional before filing.

Yes — when the methodology aligns with the standards documented in IRS Publication 5653 and the Cost Segregation ATG. The IRS does not specify who must perform a cost segregation study; it specifies what makes a study defensible: an engineering-based component analysis, supporting documentation for each classification, schedules a CPA can file, and a methodology the taxpayer can produce on audit.

CostSegX reports include all four. The methodology section cites IRC §168 (depreciation), Rev. Proc. 87-56 (asset class lives), and the relevant Pub 5653 sections. The component analysis documents how each portion of basis was classified. The Form 3115 package (for look-back studies on properties placed in service in prior years) follows DCN 7 — the IRS's automatic-consent accounting method change that requires no IRS approval and no user fee.

See our methodology page for the full IRS-citation walkthrough, or read the IRS ATG directly.

We're built for the residential 1–4 unit segment. Outside that scope, traditional firms exist for a reason — recommend you use one.

We refer out-of-scope properties to credentialed engineering firms. Email us with the property and we'll send the right firm.

Enter an address. The AI fetches public records. We estimate your Year-1 cost segregation deduction. No signup, no payment.

Run my free estimateFree estimate · No signup · Full study $499 if you proceed

Specific guides for the most common cost segregation scenarios.

How short-term rental hosts combine the STR loophole with cost segregation to offset W-2 income — if they qualify.

Accessory dwelling unit cost segregation: detached, attached, and converted ADUs. OBBBA bonus depreciation eligibility.

How the engine classifies components per IRS Pub 5653, IRC §168, and the Cost Segregation ATG.